Bandwidth Hawk

While officials have claimed billions of dollars in savings thanks to BEAD changes, the program’s full sum remains appropriated by Congress.

By: Steven S. Ross, Broadband Communities

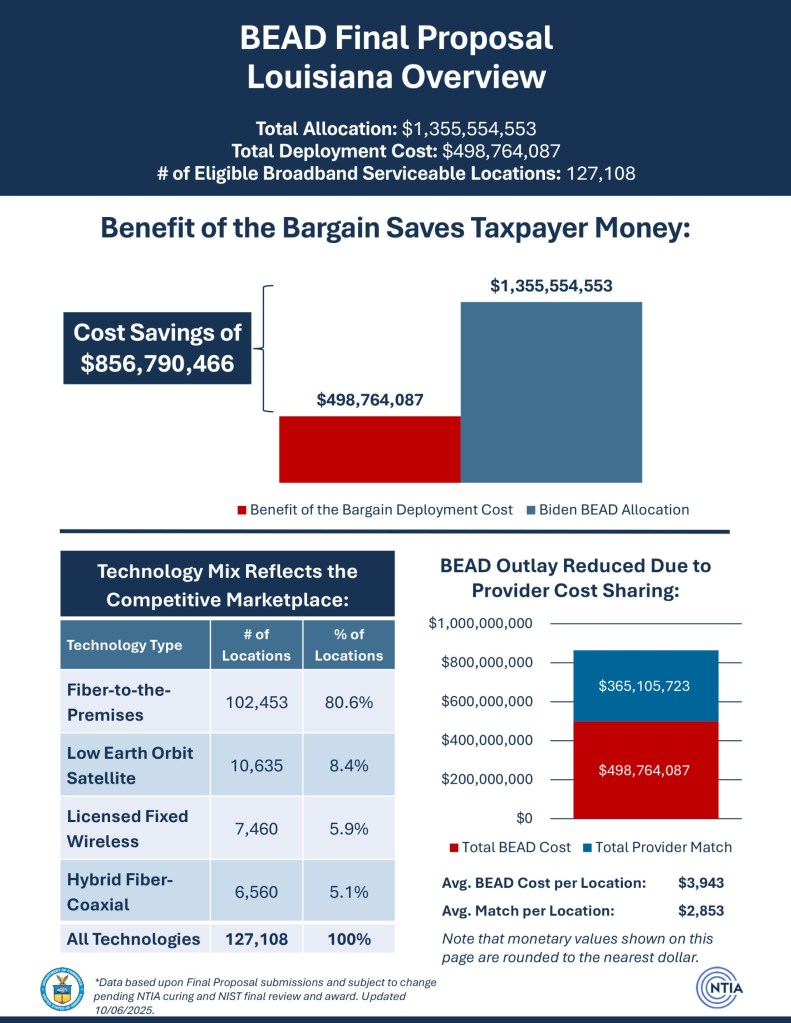

With about three quarters of all final proposals for the Broadband Equity, Access, and Deployment (BEAD) Program now approved, it appears so far that the yearlong enforced review and delay saved $462,305,075.

That’s just over 1 percent of the original BEAD appropriation of $42.45 billion.

Meanwhile, as officials have claimed billions in savings thanks to BEAD’s Benefit of the Bargain, the full sum of the program remains appropriated by Congress.

Congress has not publicly considered rescinding it in whole or in part (the remaining pot of money has been vaguely promised by the Department of Commerce to states for other communications-related uses). In actuality, the lengthy review so far has trimmed original funds requested by the 42 eligible entities (states and territories) to have their final proposal approved thus far by just 3.8 percent, from $12,130,783,703 to $11,668,478,628.

The overall number of locations to be served in these states and territories declined slightly, to 2,694,413 from the midsummer tally of 2,766,862 (California is missing from both lists).

All of the decline was borne by low-earth-orbit (LEO) satellite services, presumably because some of the LEO deployments originally approved by states were built with private funds while waiting for NTIA final approval. That’s consistent with the overall increase in cost served per location I calculated ($4,331 in the 42 final proposals approved so far, versus $4,217 for the same states and territories in the original proposals).

LEO initial grant-eligible costs are low, but eventual monthly service charges are expected to be higher.

In its plan revisions, the National Telecommunications and Information Administration (NTIA) combines all BEAD-serviceable locations (BSLs) with what it describes as “some” community anchor institutions (CAIs) to sidestep tweaks we noted last year in individual state definitions.

Last summer, I calculated $4,725 per what seemed to be any eligible location on the Federal Communications Commission broadband maps. So don’t consider any of these costs-per-location as rigidly accurate. There’s a more complete explanation below.

BEAD originally was planned mainly as a fiber-to-the-premises deployment. But a lot of fiber got built without federal aid. Also, LEO technology matured. LEO garnered more than 20 percent of all service to premises in the Benefit of the Bargain round.

The overall pattern has held, so far, in final NTIA approvals, with fiber still dominating despite Commerce Secretary Howard Lutnick’s frequent complaints that the original Biden plan, by favoring fiber, raised costs alarmingly and thus had to be changed.

That all adds up to much ado about nothing when we talk about federal appropriations and development plans – barely a rounding error and likely failing to keep up with inflation in the construction industry last year. But the list of 14 states and territories still under review by NTIA is particularly heavy in blue states – ones that have been voting Democratic. So it will be interesting to see if the benign pattern holds.

Eligible entities with final BEAD proposals still to be released:

- Alaska

- California

- District of Columbia

- Illinois

- Mississippi

- New Mexico

- Oklahoma

- Oregon

- Pennsylvania

- Puerto Rico

- Tennessee

- United States Virgin Islands

- Vermont

- Washington

NTIA has tried to make something out of nothing by comparing the much higher original state-by-state “Biden” appropriations to its final-plan numbers. But by last July, the 42 states that eventually got their plans approved (with minor modifications) had left $18.3 billion on the table of the original $30.4 billion allocated specifically to them by BEAD in 2021. Will they get to keep it, as promised by Commerce Secretary Howard Lutnick?

A typical NTIA summary sheet for a state final approval.

And will the national media even notice if they don’t? The New Yorker, for instance, used 10 pages to explore Lutnick’s role in the White House’s tariff policy and never mentioned his thumb on the BEAD scale while making room to describe at least four meals enjoyed by the author. As big as BEAD is for our industry and our customers, it is barely noticeable to others amid other federal issues.

Where the funds will go

As noted, LEO deployments approved by NTIA declined in the 42 state and territorial plans with final approvals so far. Fiber gained slightly. The biggest winners were point-to-point wireless (gaining about 34,000 locations) and legacy hybrid fiber-coax (gaining about 40,000 locations).

Proportion of fiber in the mix increased:

| Fiber % | LEO % | Wireless % | HFC & Others % | |

| Final Approvals | 65.6% | 21.1% | 10.9% | 2.3% |

| Preliminary Approvals | 63.6% | 21.1% | 9.4% | 0.8% |

Locations to be served:

| Fiber | LEO | Wireless | HFC & Others | |

| Final Approvals | 1,766,937 | 569,474 | 294,366 | 61,598 |

| Preliminary Approvals | 1,760,588 | 612,560 | 260,941 | 22,981 |

Defining “locations”

As I noted last September, a broadband serviceable location (BSL) is defined by NTIA and the Federal Communications Commission (FCC) as a residential or business structure that has or can potentially receive fixed broadband service. BSLs are ranked for BEAD eligibility in tiers on the FCC broadband map.

After states decide what tier might describe a BSL best, they can be challenged by service providers, local governments, end-users, and so forth. But not all structures are considered BSLs.

Uninhabitable buildings and many community anchor institutions (CAIs) like public works buildings, libraries, police departments, and courts are typically excluded from the BSL count, even if they need more broadband service than they have and even if providers want to provide such service. There are also enterprise-level businesses (ELBs) which generally are not BEAD eligible; they are supposedly big and rich enough to take care of themselves.

National rules define them as typically having at least 250 employees and international reach. Many rural agriculture-based businesses qualify.

All this led to a mismatch between NTIA’s own list of BSLs and CAIs versus state counts in BEAD proposals. In approving the final round, NTIA gave up and just enumerates “BSLs including some CAIs” in its final state plan approvals.

Steve Ross can be reached at steve@bbcmag.com.