Bandwidth Hawk

With proposed deployment plans now mostly submitted, fiber is still a big winner in Broadband Equity, Access, and Deployment (BEAD) funding.

By: Steven S. Ross, Broadband Communities

With BEAD proposals now largely submitted, representing $18 billion of the $41.6 billion appropriated for their use by Congress, fiber has still emerged as the technology of choice for over 2.2 million (at least 64%) of broadband serviceable locations (BSLs).

Two Low-Earth-orbit (LEO) satellite providers snagged at least 770,000 BSLs (22%), terrestrial wireless collected 340,000 BSLs (almost 10%), and hybrid fiber-coax (HFC) picked up 35,000 BSLs (1%).

Meanwhile, California still has until November 21 to propose how they’ll allocate funds to reach their BSLs.

The cost in California is expected to be about 3% of the national total, even though California has more than a tenth of the nation’s population.

The reason? California had more connected premises in the first place.

There are also some definitional uncertainties that suggest fiber’s lead is even greater. More on that as well, below.

This Hawk column updates and expands upon my September 2 column, which covered 11 states.

In terms of funds allocated, Comcast (roughly $800 million as of mid-September) and AT&T (close to $600 million) seem to lead the pack.

Ranked by premises served, SpaceX is the clear leader with Kuiper not far behind. SpaceX charges more (typically $1,500 per BSL versus roughly $1,000 per BSL for Kuiper), but SpaceX actually exists. Kuiper, however, is not operational at the scale of the BSLs it has won in state proposals – around 300,000.

Table: Confusion between states and NTIA on what premise is a BSL and what are CAIs (community anchor institutions).

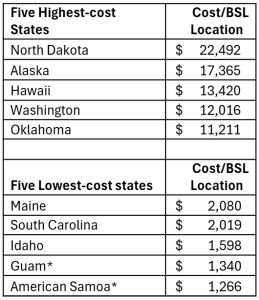

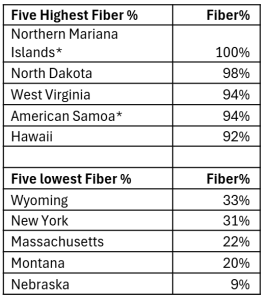

Thus, the national pattern holds true for the federal government’s per-premises cost to supply broadband – about $5,000 per premise, and under $7,000 per premise served by fiber. That’s in line with other federal broadband grant programs, such as ReConnect at the U.S. Department of Agriculture. But the average hides a wide range in average costs by state and federal territory. That range is emphatically not due exclusively to how many premises are served by fiber (see tables below).

I’ll discuss some of the state-to-state oddities later, but I do want to get to the muddled definitions for various types of premises needing broadband.

Interpreting the numbers

The National Telecommunications and Information Administration (NTIA) defines a BSL as a residential or business structure that has or can potentially receive fixed broadband service. BSLs are ranked for BEAD eligibility in tiers on the Federal Communications Commission (FCC) broadband map, but the tiers can (as most readers know) be challenged by interested parties. Unserved BSLs are those that lack reliable service at least 25 Mbps downstream and 3 Mbps upstream. BSLs with some access but broadband service less than 100 Mbps downstream and 20 Mbps upstream are “underserved.”

After states decided what tier a BSL might fit into, the state definitions were challenged by service providers, local governments, end-users, and so forth. The revised list was then used by states to define grant project areas eligible for BEAD funding.

But not all structures are considered BSLs. Uninhabitable buildings and many community anchor institutions (CAIs) like public works buildings, libraries, police departments, and courts are typically excluded from the BSL count, even if they need more broadband service than they have and even if providers want to provide such service to help justify adding more infrastructure for regular BSLs.

This has led to a mismatch between NTIA’s own list of BSLs and CAIs versus state counts in BEAD proposals.

What’s more, enterprise-level businesses (ELBs) are not generally supposed to be counted for BEAD, either. The theory is that they are big and rich enough to take care of themselves. The normal national rules define them as large organizations, typically with more than 250 employees and complex organizational structures.

In most federal programs, ELBs are often national or global. But in rural areas, many farms may meet this definition. And now, due to active data centers being built where the power is available to run them – often in rural areas – there is more muddling.

Back to the data

Considering the aforementioned details, it is little wonder that NTIA and the states have been a bit inconsistent about CAIs and ELBs. I count a bit more than 3.5 million BSLs from state submissions. NTIA’s website counts 3.3 million. All of that difference seems to be due to NTIA not counting CAIs. Furthermore, the ELB issue separately lurks in the background.

Aside from California, Oklahoma had (as of October 20) yet to fully define about 10,000 premises as BSLs, CAIs, or ELBs. Also, many terrestrial wireless projects will serve an undefined or fuzzy number of households. The HFC share also seems low, given that Comcast is still (pending review) the largest single fund winner. But at least some of the new Comcast builds seem to be pure fiber. Also, more than half of all the HFC builds proposed for the whole country so far are concentrated in just four states – Louisiana, Pennsylvania, Texas, and Virginia.

Among U.S. territories, the picture is also mixed.

Puerto Rico has been connecting all its premises under an earlier program and has proposed using much of its BEAD allocation for storm-proofing. Same with the U.S. Virgin Islands.

Similarly, American Samoa and Guam want to do the same and only see connecting about 10,000 premises between them.

The BEAD bargain

In theory, the $21 billion in currently unallocated BEAD money (roughly $20 billion after California finishes its plans) will go to the individual states. That’s what was promised when Commerce Secretary Howard Lutnick halted what had been an on-schedule program and caused what I correctly predicted last April would be a year’s delay.

But the federal shutdown has increased White House talk (and action), with unilateral recissions of money that, like for BEAD, has already been appropriated. The full Supreme Court has yet to rule on that and will likely not rule until January at the earliest. I would not be surprised to see the “bargain” funds swallowed by the immediate need (both financial and face-saving) to help with health insurance costs and control of the deficit.

True, the states that would be most affected by a BEAD recission would be those who voted for President Trump in the 2024 election. But most farmers are in red states as well… and THEY need help, especially for handling China’s abandonment of soybean purchases in the U.S. as part of the ongoing tariff war.

Back in August, I suggested states use some of the money to guarantee loans to deployers who otherwise would be paying higher interest rates or who found themselves unable to raise money for unforeseen construction delays. I still think that’s a good idea, and one that seems more and more important with each passing month.

Is there enough spectrum to handle the proposed 770,000 new LEO customers, along with existing customers and more to come in California? I’m not sure. That works out to almost 250 more households per county. The general rule now is that any one satellite within view can handle about 10 customers at the same time. “On average” it won’t work, but rural areas should beat the average easily. What about 10 years from now? BEAD was supposed to be a permanent problem-solver. It may not be.

You can reach Steve Ross, the Bandwidth Hawk, at steve@bbcmag.com.